All Categories

Featured

Table of Contents

A PUAR allows you to "overfund" your insurance coverage right approximately line of it ending up being a Modified Endowment Contract (MEC). When you use a PUAR, you swiftly raise your money worth (and your survivor benefit), thus boosting the power of your "financial institution". Further, the more cash money worth you have, the higher your interest and reward payments from your insurance provider will certainly be.

With the surge of TikTok as an information-sharing system, monetary guidance and strategies have discovered a novel means of dispersing. One such technique that has been making the rounds is the boundless financial idea, or IBC for brief, gathering recommendations from celebs like rapper Waka Flocka Fire. Nevertheless, while the approach is presently popular, its roots trace back to the 1980s when economic expert Nelson Nash introduced it to the globe.

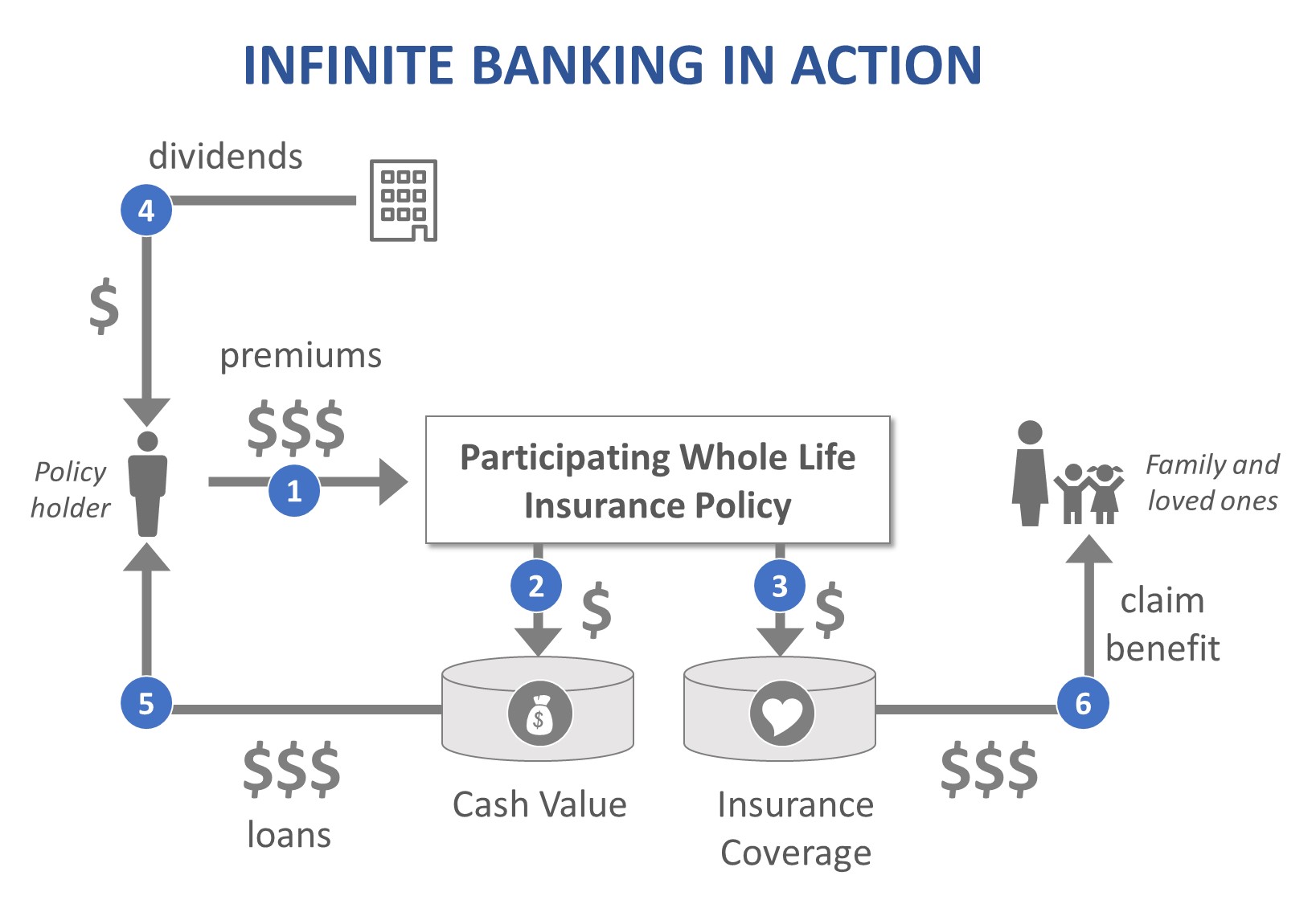

Self-financing With Life Insurance

Within these policies, the cash money value grows based on a price set by the insurance company (Borrowing against cash value). As soon as a substantial cash money value builds up, insurance holders can get a cash worth financing. These finances vary from standard ones, with life insurance policy functioning as collateral, implying one might lose their protection if borrowing exceedingly without adequate cash value to support the insurance policy expenses

And while the appeal of these plans appears, there are inherent constraints and risks, requiring diligent cash value monitoring. The strategy's legitimacy isn't black and white. For high-net-worth people or company owner, especially those utilizing methods like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and compound growth can be appealing.

The allure of unlimited banking doesn't negate its challenges: Expense: The foundational need, a long-term life insurance policy policy, is pricier than its term equivalents. Qualification: Not every person receives whole life insurance coverage because of rigorous underwriting procedures that can omit those with details health and wellness or way of life problems. Complexity and danger: The intricate nature of IBC, paired with its risks, might deter many, especially when easier and less dangerous choices are available.

How secure is my money with Financial Leverage With Infinite Banking?

Alloting around 10% of your monthly earnings to the policy is just not possible for lots of people. Making use of life insurance policy as a financial investment and liquidity source needs discipline and surveillance of policy money worth. Get in touch with a financial advisor to identify if boundless financial lines up with your priorities. Part of what you check out below is just a reiteration of what has already been said above.

So prior to you obtain right into a situation you're not gotten ready for, know the adhering to first: Although the idea is typically offered thus, you're not really taking a lending from on your own. If that were the instance, you would not need to repay it. Instead, you're borrowing from the insurer and have to repay it with passion.

Some social media sites posts advise making use of cash value from whole life insurance coverage to pay for credit card financial debt. The concept is that when you repay the car loan with interest, the amount will be sent back to your investments. Sadly, that's not exactly how it functions. When you pay back the finance, a section of that passion mosts likely to the insurance provider.

For the initial numerous years, you'll be repaying the compensation. This makes it extremely difficult for your plan to accumulate worth during this time. Entire life insurance policy expenses 5 to 15 times much more than term insurance coverage. Lots of people simply can not manage it. So, unless you can manage to pay a few to a number of hundred bucks for the following years or even more, IBC will not work for you.

What is the minimum commitment for Policy Loans?

If you require life insurance, here are some important tips to take into consideration: Take into consideration term life insurance policy. Make certain to shop around for the finest rate.

Visualize never needing to bother with financial institution finances or high rates of interest once more. Suppose you could obtain cash on your terms and build riches all at once? That's the power of limitless financial life insurance policy. By leveraging the money value of whole life insurance policy IUL policies, you can expand your wide range and borrow cash without depending on typical financial institutions.

There's no set lending term, and you have the flexibility to choose on the repayment timetable, which can be as leisurely as paying back the car loan at the time of death. Cash flow banking. This adaptability reaches the servicing of the finances, where you can choose interest-only payments, keeping the loan equilibrium flat and convenient

Holding cash in an IUL fixed account being credited passion can usually be better than holding the money on deposit at a bank.: You've constantly desired for opening your own bakery. You can borrow from your IUL policy to cover the initial costs of renting out an area, acquiring equipment, and working with team.

Who can help me set up Borrowing Against Cash Value?

Personal financings can be acquired from standard banks and lending institution. Right here are some bottom lines to consider. Credit score cards can supply a flexible method to borrow money for extremely short-term periods. Borrowing cash on a credit rating card is typically really costly with annual portion rates of passion (APR) often reaching 20% to 30% or more a year.

{kind=link}

Latest Posts

Infinite Banking Concept Scam

Bring Your Own Bank: Expanding The Ways Companies ...

Build Your Own Bank